GREENSBORO, N.C. — Data breaches, identity theft, it all sounds like…

*********

….white noise and the TV static you want to turn off. Until of course, it happens to you.

One of your fellow 2WTK viewers messaged me:

Somebody got a credit card in my name and are ruining my credit. What do I do?

Ugh. This stinks. And I’m sorry. Gather yourself together.

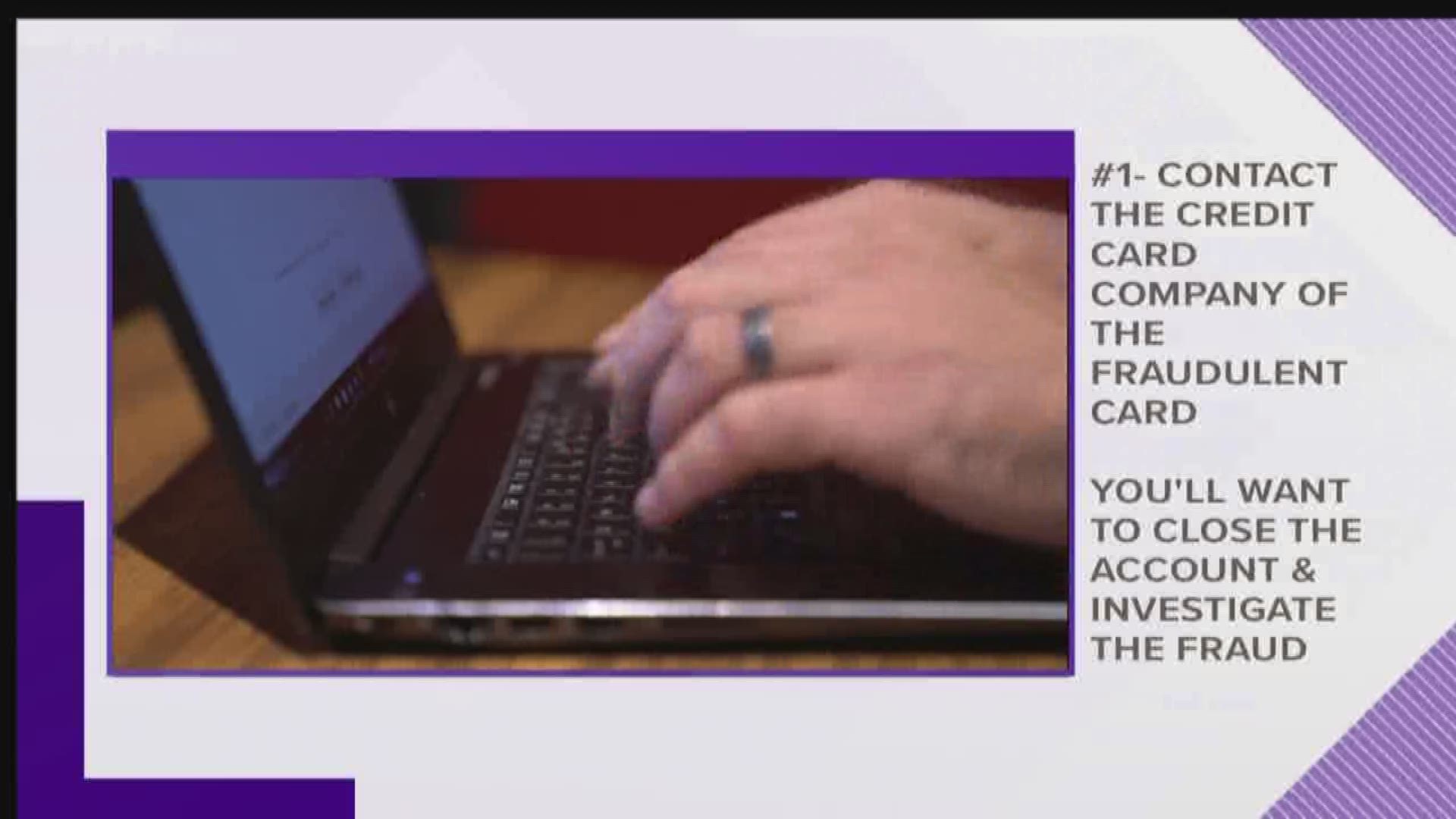

#1 Contact the credit card company of the fraudulent card.

You'll want to close the account and have them investigate the fraud. (Side note here, if you got an email or a letter, you might think you should just call the number provided, but it's always safer to look up the company's website and find the customer service number listed.)

#2 Report your identity theft with the Federal Trade Commission. They have resources to help you figure out what your next step is, credit card ID theft and bank account or tax ID theft will have different steps.

Chances are, no matter what kind of fraud, the recommendation will include a freeze on your credit. A credit freeze ALLOWS YOU to use your credit and debit card, but it keeps others from opening up accounts in your name!

CREDIT FREEZE

A credit freeze is the single, most effective way to protect against credit fraud.

"Most creditors need to see your credit report before they issue you new credit. But if you have a freeze on your account, they can't pull your file –– and may not extend you credit –– which should stop fraudsters,” explains a Consumer Report expert.

You need to contact each of the bureaus individually, doing just one isn’t enough protection. When you ask for a freeze online, it’s free. Click on each of the bureaus for the online form.

NOTE: You can temporarily “thaw” your freeze so you can get a car loan or a credit card. To do that you’ll need to get a PIN from each of the bureaus. Often, they do this by mail. And if you lose your PIN they can charge you to get it back.

The downside is a freeze can also shut out companies you want to do business with. So, if you're in the market for a car or a home loan or even a new cell plan, take care of it before you institute the freeze.